Real estate transfer tax & Table for federal states – Whenever a property or part of a property is purchased in Germany, real estate transfer tax is incurred. But, how much trade tax is incurred with the real estate purchase? The amount of the tax is determined by the individual federal states. As a rule, the real estate transfer tax ranges between 3.5 percent and 6.5 percent, depending on the federal state in which the property or land is located. For a quick orientation, we have summarized the land transfer tax rates for all 16 federal states with example purchase prices of 1 – 5 million Euros, from Bavaria to Hamburg. Back to German Real Estate Overview.

Additionally, in the following there may be slight grammatical errors, as this article was written by a German tax expert. This does not detract from the quality of information.

Grundwerbsteuer Explained: Purchase of Land or Property

As described in the introduction: Whenever a property or part of a property is purchased, land transfer tax is incurred in Germany. The tax is levied on the basis of the Land Transfer Tax Act (GrEStG). The amount of the real estate transfer tax is determined by the federal states. It is therefore a state tax. The respective federal state can therefore decide for itself whether it passes on the tax levied to its local authorities. But first we look at what a Grunderwerbsteuer really even is.

Are you looking at investing in German real estate? Don’t miss our article

Grunderwerbsteuer is a tax on the purchase of real estate. The translation of Grunderwerbsteuer is real estate transfer tax or land transfer tax. Note, in the USA, this concept has different meanings depending on the state (more on that in our article on Real Estate Transfer Tax in the US). How the Grunderwerbsteuer works is explained further below.

Who pays the Real Estate Transfer Tax?

After you have bought your property, the purchase must still be notarized. The purchase contract states who has to pay the land transfer tax: buyer or seller. Without this additional agreement, the law (§13 No. 2 GrEStG) states that first of all the previous owner and the purchaser are tax debtors, i.e. both together, buyer and seller.

After notarization, the notary sends the signed purchase contract to the responsible tax office, which then writes to the party to be charged with the real estate transfer tax assessment. The tax is due one month after notification of the tax assessment. However, the tax office may set a longer payment deadline if necessary (see Grunderwerbsteuergesetz (GrEStG) §15 Due date of the tax).

Grundwerbsteuergesetz (GrEStG): § 13 Tax debtor

Here is a short look at the legal text on real esate purchases according to §13 No. 2 GrEStG. This is our best attempt at a translation, these terms are as similar as possible to the original meaning.

Tax debtors are:

By Default: the persons involved in a purchase transaction as contractual parties;

In case of acquisition by operation of law: the previous owner and the acquirer;

In the case of acquisition in expropriation proceedings: the acquirer;

In the case of the highest bid in compulsory auction proceedings: the highest bidder;

In the case of the merger of at least 95 per cent of the shares in a company in the hands of the acquirer: the acquirer;

In case of acquisition by several companies or persons: these parties;

In the event of a change in the membership of a partnership: the partnership;

In the case of an economic interest of at least 95 per cent in a company: the legal entity which holds the economic interest.

Source: Federal Ministry of Justice (as of 09/2020).

Cost table: Tax According to Purchase Price

Status: 09/2020

Tax Rate by State: Amount

Bavaria – 3,50%

Berlin – 6,0%

Bremen – 5.0%

Hessen – 6.0%

Lower Saxony – 5.0%

Rhineland-Palatinate – 5.0%

Saarland – 6.50% li>

Saxony – 3,50%

Saxony-Anhalt – 5.0%

Property Tax Compared to Trade Tax, Income Tax and Sales Tax

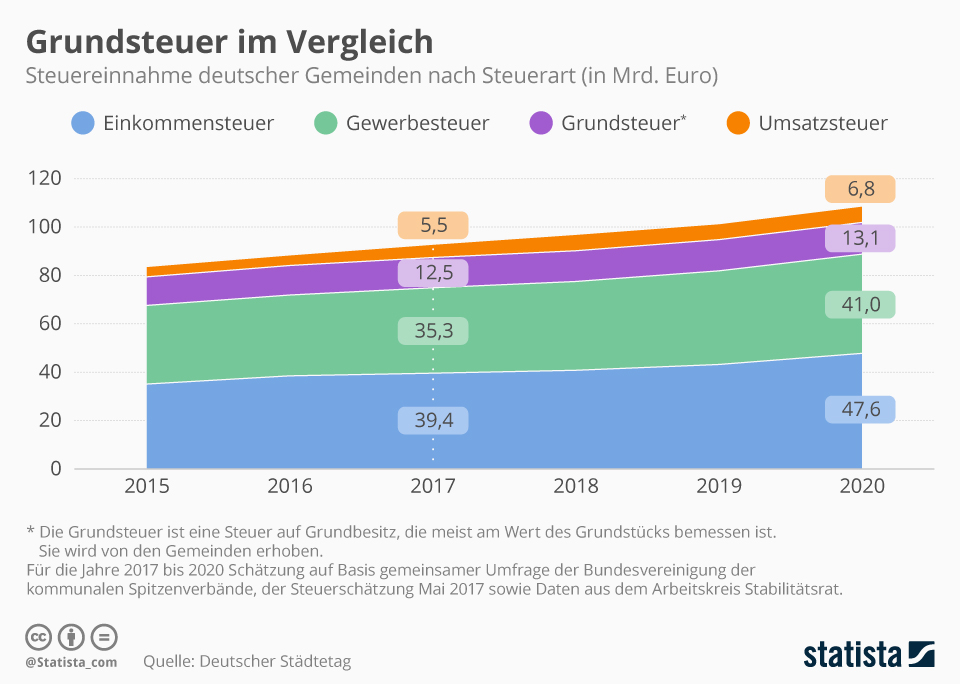

Real estate tax is levied on land, but also on hereditary building rights to land, the so-called substance tax. The assessment basis for the land tax is usually the value of the land plot. The tax rate is usually set at the municipal level.

This infographic below shows the tax revenue of German municipalities according to tax types (in billions of Euros). Please note that an English translation was not available. Blue denotes income tax, green is trade tax, purple is property tax, and orange is goods-and-services tax.

Purchase Price – 1.000.000 Euro

Below a graph for the amount of taxes you will pay based on what state you are buying the property in. The basis is a purchase price of 1 million Euro.

Baden-Württemberg

5.00%

50.000,00 €

Bavaria

3.50%

35.000,00 €

Berlin

6.00%

60.000,00 €

Brandenburg

6.50%

65.000,00 €

Bremen

5.00%

50.000,00 €

Hamburg

4.50%

45.000,00 €

Hessen

6.00%

60.000,00 €

Mecklenburg-Western Pomerania

6.00%

60.000,00 €

Lower Saxony

5.00%

50.000,00 €

North Rhine-Westphalia

6.50%

65.000,00 €

Rhineland-Palatinate

5.00%

50.000,00 €

Saarland

6.50%

65.000,00 €

Saxony

3.50%

35.000,00 €

Saxony-Anhalt

5.00%

50.000,00 €

Schleswig-Holstein

6.50%

65.000,00 €

Thuringia

6.50%

65.000,00 €

Purchase Price – 1.200.000 Euro

Below a graph for the amount of taxes you will pay based on what state you are buying the property in. The basis is a purchase price of 1.2 million euros.

Baden-Württemberg

5.00%

60.000,00 €

Bavaria

3.50%

42.000,00 €

Berlin

6.00%

72.000,00 €

Brandenburg

6.50%

78.000,00 €

Bremen

5.00%

60.000,00 €

Hamburg

4.50%

54.000,00 €

Hessen

6.00%

72.000,00 €

Mecklenburg-Western Pomerania

6.00%

72.000,00 €

Lower Saxony

5.00%

60.000,00 €

North Rhine-Westphalia

6.50%

78.000,00 €

Rhineland-Palatinate

5.00%

60.000,00 €

Saarland

6.50%

78.000,00 €

Saxony

3.50%

42.000,00 €

Saxony-Anhalt

5.00%

60.000,00 €

Schleswig-Holstein

6.50%

78.000,00 €

Thuringia

6.50%

78.000,00 €

Purchase Price – 1.500.000 Euro

Below a graph for the amount of taxes you will pay based on what state you are buying the property in. The basis is a purchase price of 1.5 million euros.

Baden-Württemberg

5.00%

75.000,00 €

Bavaria

3.50%

52.500,00 €

Berlin

6.00%

90.000,00 €

Brandenburg

6.50%

97.500,00 €

Bremen

5.00%

75.000,00 €

Hamburg

4.50%

67.500,00 €

Hessen

6.00%

90.000,00 €

Mecklenburg-Western Pomerania

6.00%

90.000,00 €

Lower Saxony

5.00%

75.000,00 €

North Rhine-Westphalia

6.50%

97.500,00 €

Rhineland-Palatinate

5.00%

75.000,00 €

Saarland

6.50%

97.500,00 €

Saxony

3.50%

52.500,00 €

Saxony-Anhalt

5.00%

75.000,00 €

Schleswig-Holstein

6.50%

97.500,00 €

Thuringia

6.50%

97.500,00 €

Purchase Price – 2.000.000 Euro

Below a graph for the amount of taxes you will pay based on what state you are buying the property in. The basis is a purchase price of 2 million euros.

Baden-Württemberg

5.00%

100.000,00 €

Bavaria

3.50%

70.000,00 €

Berlin

6.00%

120.000,00 €

Brandenburg

6.50%

130.000,00 €

Bremen

5.00%

100.000,00 €

Hamburg

4.50%

90.000,00 €

Hessen

6.00%

120.000,00 €

Mecklenburg-Western Pomerania

6.00%

120.000,00 €

Lower Saxony

5.00%

100.000,00 €

North Rhine-Westphalia

6.50%

130.000,00 €

Rhineland-Palatinate

5.00%

100.000,00 €

Saarland

6.50%

130.000,00 €

Saxony

3.50%

70.000,00 €

Saxony-Anhalt

5.00%

100.000,00 €

Schleswig-Holstein

6.50%

130.000,00 €

Thuringia

6.50%

130.000,00 €

Purchase Price – 2.500.000 Euro

Below a graph for the amount of taxes you will pay based on what state you are buying the property in. The basis is a purchase price of 2.5 million euros.

Baden-Württemberg

5.00%

125.000,00 €

Bavaria

3.50%

87.500,00 €

Berlin

6.00%

150.000,00 €

Brandenburg

6.50%

162.500,00 €

Bremen

5.00%

125.000,00 €

Hamburg

4.50%

112.500,00 €

Hessen

6.00%

150.000,00 €

Mecklenburg-Western Pomerania

6.00%

150.000,00 €

Lower Saxony

5.00%

125.000,00 €

North Rhine-Westphalia

6.50%

162.500,00 €

Rhineland-Palatinate

5.00%

125.000,00 €

Saarland

6.50%

162.500,00 €

Saxony

3.50%

87.500,00 €

Saxony-Anhalt

5.00%

125.000,00 €

Schleswig-Holstein

6.50%

162.500,00 €

Thuringia

6.50%

162.500,00 €

Purchase Price – 5.000.000 Euro

Below a graph for the amount of taxes you will pay based on what state you are buying the property in. The basis is a purchase price of 5 million euros.

Baden-Württemberg

5.00%

250.000,00 €

Bavaria

3.50%

175.000,00 €

Berlin

6.00%

300.000,00 €

Brandenburg

6.50%

325.000,00 €

span>

5.00%

250.000,00 €

Hamburg

4.50%

225.000,00 €

Hessen

6.00%

300.000,00 €

Mecklenburg-Vorpommern

6.00%

300.000,00 €

Lower Saxony

5.00%

250.000,00 €

North Rhine-Westphalia

6.50%

325.000,00 €

Rhineland-Palatinate

5.00%

250.000,00 €

Saarland

6.50%

325.000,00 €

Saxony

3.50%

175.000,00 €

Saxony content

5.00%

250.000,00 €

Schleswig-Holstein

6.50%

325.000,00 €

Thuringia

6.50%

325.000,00 €

Plots, apartments & house in Germany. Classical or exotic: Which property is suitable as an investment? The interview: Real estate as a capital investment. In our city analysis you will find clues as well (see below).

Tip from the real estate agent: You want a purchase price for comparison? Before you evaluate your real estate , use apps from real estate portals. Here you can simply track your location with GPS and the app will show you purchase prices and comparison offers in your area. The fast way to a first, rough evaluation of your property.

Price: Rent, buy, living

Renting, buying, living. Here you will find more information about the population, rental prices and purchase prices in the individual cities:

Tax optimization: Procedure and Knowledge Build-Up

Topic Taxes. This brings us directly to the topic of optimizing taxes. Knowledge about finances and taxes is absolutely essential when buying your first property. Understanding taxes is important, because this is how you can convert taxes into private assets.

How does it Work? An Example for Real Estate Investors

In the case of real estate, for example, this involves lifting platforms for duplex parking spaces. So lifting platforms, where you get e.g. two cars on one parking space. They have a shorter depreciation period. Here, depreciation for wear and tear applies, distributed over the actual useful life, deductible according to the official lists of the Ministry of Finance. Exception expenses up to 800 Euro – without VAT – can be deducted immediately in the year of purchase.

You will of course no longer get such knowledge from your tax consultant. Why should he or she, if he or she knew about it, your tax advisor* would be a millionaire* himself.

Details

More details on optimizing your tax sheet for your real estate can be found in our article on the matter

https://lukinski.com/wp-content/uploads/2020/08/fertighaus-bau-aufbau-kran-3-tage-garage-carport-3-etagen-spitzdach-grundstuck-muenchenbaustelle.jpg9601280Laurahttps://lukinski.com/wp-content/uploads/2024/04/lukinski-logo-real-estate-investment-germany-house-villa-off-market.svgLaura2020-11-03 09:57:392022-04-03 08:15:38Grunderwerbsteuer – Meaning, Translation, Explanation of German Real Estate Tax

of the ownership of a property")