Self-disclosure for the bank – You want to buy a property and this is to be financed by a German bank? More on Real Estate Germany. Whether Sparkasse, Volksbank, private banks, Postbank, Deutsche Bank or Commerzbank, banks want creditworthiness (risk minimization) and proof of it. This proof is called self-disclosure. Here you present your assets and your monthly income. In addition, you give the bank information about the property and the financing structure.

The self-disclosure is a proof of your creditworthiness. It includes your monthly income, expenses, assets and liabilities. The self-disclosure is completed either by you, as the sole applicant, or with a second borrower, your co-applicant.

Download: Free Template

There is no official self-disclosure, for example from the tax office. The form and contents are freely selectable.

Here you can find the self-disclosure free of charge, as a good and complete PDF and Word template:

Before you get to know the individual steps, here is an overview of the structure of the (or this) self-disclosure.

Personal data and activity

Monthly income and expenditure

Assets and liabilities

Object to be financed and financing structure (repayment)

Consent Schufa information

Annex: Proof of income

All the information you provide here comes from yourself. Hence the name of the self-disclosure. It is important, and you should always bear this in mind, that all information must be verifiable.

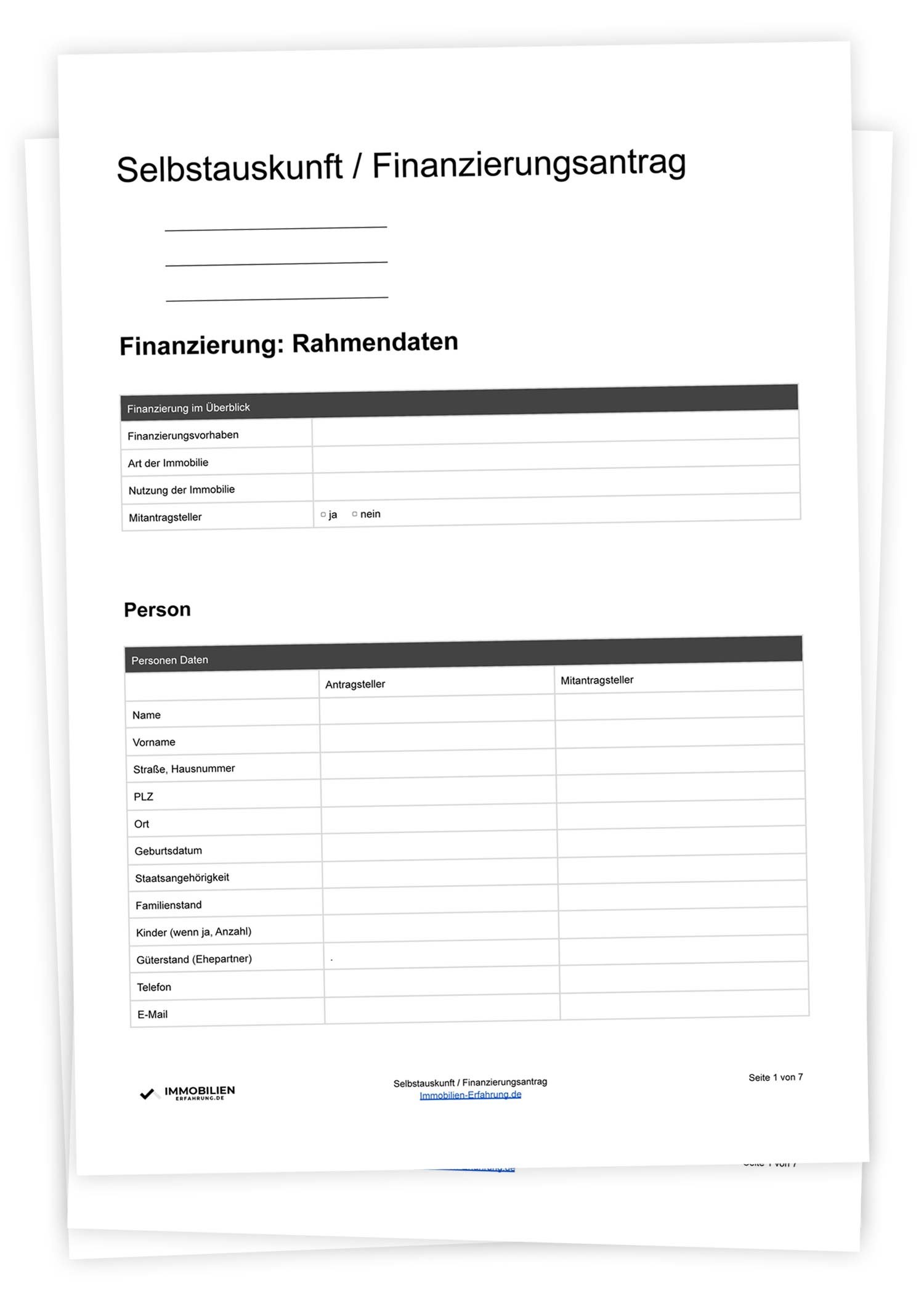

Financing in brief: framework data ‘ Step 1

To begin with, summarize the framework data of the desired financing. Really, in extremely short form!

In the second block, you provide information about your personal data. Either as the sole borrower or together with your co-applicant.

Personal details

Activity data

Credit rating: Income – Step 3

From the personal data and the activity you come in step 3 to the monthly income and expenses. Here you compare both blocks and calculate the sum. Your result should be a surplus and this surplus is your financial margin.

Monthly income

Monthly income includes income from wages and salaries, but also other variable, regular sources of income.

Wage / salary (net)

Recurring monthly variable income

Income from self-employment

Pensions and annuities

Rental income (cold)

Child benefit

Maintenance

Other income

Monthly expenditure

The monthly expenses include the warm rent, or the loan, or the amount of the monthly repayment.

Housing costs; rent or loan

Will there be no housing costs in future: Yes / no?

Health insurance

Other insurance (pension, building society, life insurance, etc.)

Cost of living

Loans

Leasing

Liabilities

Child support obligations

Other expenditure

Net worth (assets / liabilities) – Step 4

After listing your regular, recurring income and expenses, here is a list of your assets and liabilities.

Again, let’s take a quick look at an example of what belongs in the listing. Let’s start with the assets:

Calculate credit

In the section on assets and credit balances, list the following assets:

Bank and savings accounts

Securities (market value)

Insurance policies (surrender value)

Real estate assets

Building savings balance

Other assets

Calculate liabilities

On the liabilities side, then:

Bank, instalment and leasing loans

Guarantees

Other liabilities

Real estate and financing: Use of credit – Step 5

In the penultimate, fifth step, you give your banker an overview of the property and the financing structure (repayment).

Property

First give your bank an insight into the property to be financed. Purchase price, type of property, type of use, here is all the important information for your bankers.

Exact address (street, house number, postal code and city)

Type of use

Year of manufacture

Real estate type

Living space (m²)

Plot (m²)

Commercial (m²)

Rented (m²)

Undeveloped area (m²)

Construction

State

Last modernization (year)

Pitches

Room (for apartment)

Residential unit (no. according to declaration of partition)

Location in the object (for apartment)

Special features

Financing structure and loan amount

After you have described your financing wish, it goes to the amount and the repayment of the financing.

Purchase price

Property

Conversion / Modernization

Building costs (house)

Outdoor facilities

Incidental building costs

Real estate transfer tax

Own contribution

Outdoor facilities

Notary and land register

Real estate agent

Inventory

Financing costs

In the area of loans:

Amount

Debit interest rate

Redemption

Rate

Unscheduled repayment option

Schufa information and data protection – Step 6

Last but not least, you agree to a Schufa query and the privacy policy in your self-disclosure.

Tip. Once a year you get this self-disclosure free of charge:

In each self-disclosure must be a bank account, or the banking institution. Choose a bank or a bank account of a bank with which you have a good relationship.

Tip 2: Step 5 with financial advisor

In the sixth step, you give your banker information about the property of your choice, as well as the financing structure. It is best to discuss this part with a financial advisor.

Tip 3: Accurate submission of documents

Really make sure that everything is submitted accurately, with all the important documents. If a mistake creeps in already here, this immediately reduces the chance of real estate financing by your bank.

https://lukinski.com/wp-content/uploads/2021/08/selbstauskunft-finanzierung-immobilie-wohnung-haus-mehrfamilienhaus-bank-vermoegen-einkommen-nachweis.jpg7991200L_kinskihttps://lukinski.com/wp-content/uploads/2024/04/lukinski-logo-real-estate-investment-germany-house-villa-off-market.svgL_kinski2021-08-23 13:14:182022-03-01 10:46:03Self-disclosure explained: financing at the bank for house & apartment